Is the Costa del Sol real estate market heading for a bubble?

2025 Analysis based on economic indicators & market Fundamentals

Yes, property prices are growing higher and higher, but let’s be honest, we can’t base investment decisions purely on price trends. To truly understand if the market is sustainable and safe for investment, we need to look deeper at the fundamentals.

The Costa del Sol, especially the Golden Triangle of Marbella, Estepona, and Benahavis, has seen remarkable growth over the last five years, especially in selective micromarkets.

So, one of the most frequently asked questions among investors stands:

Is the Costa del Sol real estate market heading for a bubble?

To answer this, we compare today’s market with the conditions that caused Spain’s last bubble (1995-2007) and its crash (2008-2013). Understanding these warning signs is essential to determine whether current growth is healthy or overheating.

What defines a real estate bubble? (Spain 1995-2007)

Spain’s previous bubble was driven by a dangerous mix of cheap credit, speculative

buying and construction far beyond real demand.

1. Excessive credit growth

Between 2000 and 2004, household mortgage debt in Spain increased at an extraordinary pace, rising around 20% per year according to the valuation company TINSA. By 2007, nearly 60% of all bank lending was for real estate (French Senat report, 2011), and banks routinely over-valued properties, sometimes by up to 29%, to grant higher loan-to-value mortgages (study by Martinez-Paeés & Maza, 2014).

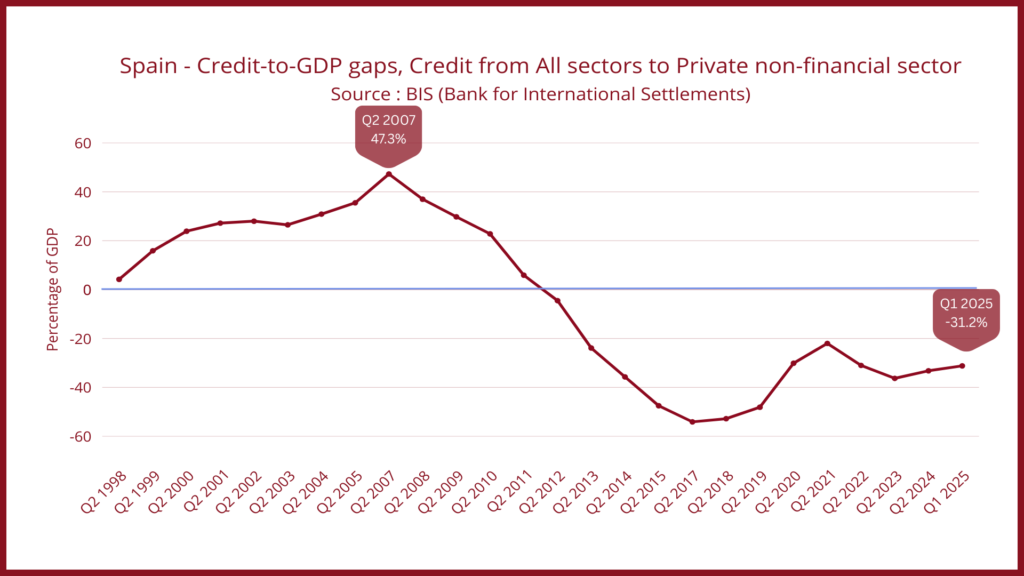

One of the clearest warning signs was the Credit Gap, which climbed to 47.3% above its long-term trend in 2007, according to the Bank for International Settlements (BIS). This indicator shows whether credit is growing unusually fast or slowly compared to the economy (GDP). At that time, credit was expanding far beyond sustainable levels, households and developers were accumulating excessive debt, and the system became highly vulnerable. When the credit gap grows excessively, the risk of a crisis increases sharply.

2. Low interest rates and risky mortgage structures

Euribor fell to around 2.4% in 2006, which made borrowing extremely cheap and encouraged households to take on large mortgages (Euribor rates.eu). Almost all of those loans, 97.9%, were variable-rate (INE). This meant that when Euribor surged in 2007-2008, monthly payments suddenly increased for millions of households. As purchasing power fell, property demand dropped, and the market correction accelerated.

3. Massive construction oversupply

During the bubble years, construction activity tripled, according to the European Central Bank. Spain was building far more homes than the population actually needed: nearly 3 million homes constructed after 2001 remained unsold. On the Costa del Sol, many coastal resort developments expanded rapidly to satisfy speculative buying rather than real residential demand. Prices in some coastal areas rose by around 250% between 1996 and 2007, forming an inflated and unstable market (TINSA).

4. GDP overdependence on construction

By 2006, construction represented nearly 12% of Spain’s GDP (Trading Economics). The economy relied too heavily on construction instead of on productive, diversified industries. This dependence made the economy fragile; once construction slowed, the entire system weakened.

5. Local corruption and poor urban planning (Marbella)

In Marbella, the years of Operacion Malaya revealed around 18,000 irregular properties built during a period of disorganised, speculative urban expansion (El Pais, 2021). Weak oversight and illegal building permits allowed uncontrolled construction, which artificially increased supply and contributed to overheating.

Do we see these indicators today? (2025)

The contrast with today could not be clearer: the main warning signs of the 1995-2007 bubble are simply not present in 2025.

Below is the indicator-by-indicator comparison.

1. Credit growth: Healthy, not excessive

Mortgage credit is growing at a moderate and sustainable pace. According to BIS data, the credit gap is currently negative, around -31% (Q1 2025), which means credit is expanding below its historical trend, indicating a more stable, and even restrictive, lending trend. Household debt stands at 43.5% of GDP, dramatically lower than the 84% recorded in 2009. There is no sign of households or developers accumulating dangerous levels of debt (see graph below).

2. Mortgage structure: much safer

Even though variable-rate mortgages are gaining popularity again, the majority of borrowers now choose fixed-rate mortgages, around 63% in 2024, providing stability even during periods of fluctuating interest rates (see graph below) (INE). With Euribor stabilised around 2.2%, the environment is far more secure than during the previous bubble, when nearly all mortgages were variable-rate and households were exposed to sudden payment increases (Euribor rates.eu).

3. Supply vs demand: A shortage, not an oversupply

Spain is currently creating approximately 240,000 new households per year, but only around 100,000 new homes are being built (Instituto Español de Analistas). Population is also 4.3 million higher than in 2007, pushing structural demand upward (Worldometer).

On the Costa del Sol, land is limited, planning is strict, and development is controlled. Supply cannot expand fast enough to meet real demographic demand. This is the opposite of the pre-crisis years, when construction outpaced real need and speculation pushed prices higher. Today’s appreciation is driven by genuine supply shortages, not speculation.

4. GDP composition: A more balanced economy

Construction now represents only about 5.3% of Spain’s GDP, less than half of what it did during the bubble (Observatorio Industrial de la Construccion). Today, growth is supported by a more diversified economy, which means housing demand is based on broader and more stable fundamentals rather than speculative forces, resulting in a healthier and more resilient market.

5. Regulatory environment: Much tougher and more controlled

Urban planning, corruption monitoring and compliance have all strengthened significantly over the last decade. The abolition of the Golden Visa in 2025, stricter rules on short-term rentals, and tighter enforcement of planning regulations have created a more disciplined environment. Speculative or irregular development is far harder to execute today than in the mid-2000s.

How about the luxury real estate market on the Costa del Sol?

The luxury real estate market is very different from the general housing market. High-end properties tend to be more resilient because most buyers rely on cash rather than credit and are motivated by lifestyle, relocation, or family needs instead of short-term speculation. On the Costa del Sol, this is clear: about 90% of buyers are international, and around 90% of transactions are completed in cash (Taylor Wimpey España).

This cash-based demand from buyers purchasing for personal use keeps the market stable and lowers the risk of a housing crash. Unlike the 1995-2007 bubble, when leverage and speculative buying pushed prices up unsustainably, the luxury market today is supported by real demand and limited supply. As a result, it is much less sensitive to interest rate changes or credit conditions and far less likely to experience the boom-and-bust cycles seen in the general housing market.

Conclusion

Based on all the indicators analysed, the Costa del Sol appears to be in a mature market driven by genuine demand and limited supply rather than in a speculative bubble. While prices in some prime locations of Marbella may appear high, the market fundamentals are very different from those of a speculative bubble.

Growth is supported by real factors:

People moving for lifestyle reasons, strong international demand, high purchasing power with mostly cash buyers, stable credit, stricter regulations and planning, limited land and carefully managed development, and an overall shortage of housing in Spain.

Unlike the pre-crisis period, the market is not inflating artificially by leverage or speculative investment. Instead, the Costa del Sol is entering a slower, healthier, and more predictable phase, supported by real demographic and economic factors rather than risky financial behaviour. For both investors and lifestyle buyers, this means that the environment is stable with long-term appreciation potential, especially in high-demand micro-markets with limited housing supply, like Marbella, and in growing markets with lower entry prices, like Estepona.

References

- BIS – Bank for International Settlements. (n.d.). Credit Gaps – Spain. Retrieved

- ECB – European Central Bank. (2019). ECB Working Paper Series No. 2245:

Household debt and real estate dynamics in Europe. - El País English Edition. (2021). Two decades later, thousands of Marbella homes

still in legal limbo. - Eurostat / Trading Economics. (2024). Spain – Residential construction indicators.

- Euribor Rates. (n.d.). Euribor long-term charts and interest rate evolution.

- INE – Instituto Nacional de Estadística. (2024). Household income statistics (2023

results). - Instituto de Analistas Financieros. (2024). Informe Económico y Financiero 2024.

- Innovando en la Construcción. (2024). Informe Construcción 2024 – Crecimiento

del sector. - Homes Overseas / Tinsa. (2007). Spanish property market: bubble dynamics and

valuation trends. - Idealista. (2025). Costa del Sol luxury market attracts buyers from 28 different

nations. - Sénat Français. (2011). Rapport d’information n° 385 (2010–2011) – La bulle

immobilière espagnole et ses effets systémiques. - Springer / Spanish Economic Review. (2015). The real estate and credit bubble:

evidence from Spain. - Worldometer. (n.d.). Spain population data.